When 90 Days of Calm Get Shattered: The Low-Volatility Breakout Signal

The S&P 500 went 90 trading days without a single move exceeding 2.85%. Then it happened. History has a name for this pattern — and a warning.

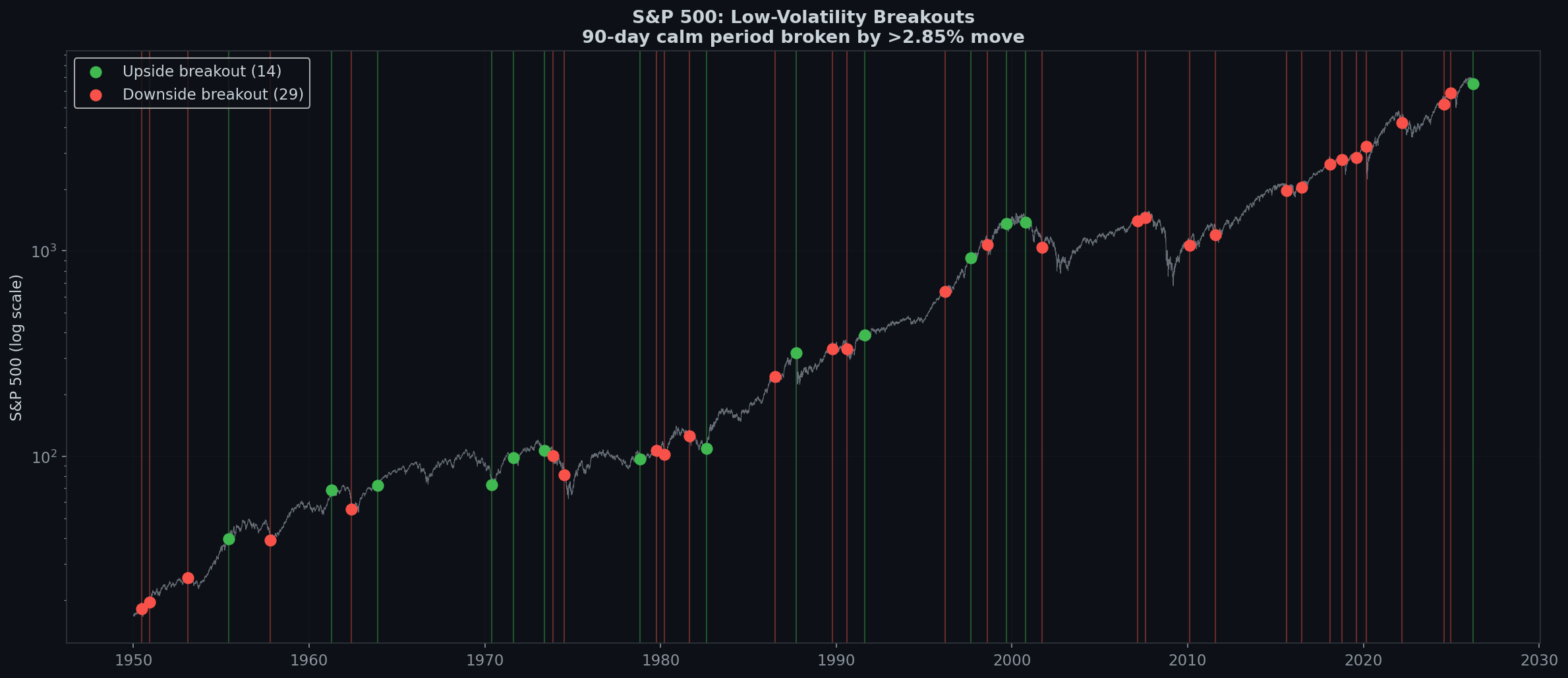

The Calm Before the Storm

On March 31, 2026, SPX didn’t just gain 2.91%. It broke a 90-day streak of contained volatility — no single session had exceeded ±2.85% in the prior three months.

We scanned every instance since 1950 where SPX went at least 90 trading days without a ±2.85% move, then broke that streak.

43 Breakouts in 75 Years

- 14 upside breakouts (calm broken by a big up day)

- 29 downside breakouts (calm broken by a big down day)

That 2:1 ratio is already telling. When a long period of calm gets shattered, it’s twice as likely to break to the downside.

Upside Breakout Forward Returns (n=14)

| Period | Average Return | Win Rate |

|---|---|---|

| 1 Day | -0.00% | 62% |

| 5 Days | +0.60% | 62% |

| 2 Weeks | +0.62% | 54% |

| 1 Month | -0.17% | 46% |

| 3 Months | +1.70% | 54% |

The 1-month forward return is negative on average (-0.17%), with a coin-flip 46% win rate. Upside breakouts don’t signal the start of a rally. They signal the end of calm and the beginning of a volatile regime.

The 1987 Case Study

September 22, 1987: SPX breaks 90 days of calm with a +2.89% upside move. Everything looks bullish. The market has been rallying all year.

October 19, 1987 (19 trading days later): Black Monday. SPX drops 20.47% in a single day.

The upside breakout wasn’t a buy signal. It was the market’s nervous system firing — an early tremor before the earthquake.

Selected Breakout Events

Notable upside breakouts:

- Aug 17, 1982 (+4.76%) — Beginning of the greatest bull run ✓

- Sep 22, 1987 (+2.89%) — 19 days before Black Monday ⚠️

- Oct 13, 2000 (+3.34%) — Dot-com crash had already begun ⚠️

- Mar 31, 2026 (+2.91%) — Today 🔍

Notable downside breakouts:

- May 28, 1962 (-6.68%) — Kennedy Slide

- Oct 13, 1989 (-6.12%) — Friday the 13th mini-crash

- Feb 24, 2020 (-3.35%) — COVID first shoe drop

- Aug 5, 2024 (-3.00%) — Yen carry trade unwind

The Boring Edge Takeaway

- When calm breaks, the direction matters less than the fact that it broke. Volatility regimes are sticky. Expect more big moves in both directions.

- Downside breakouts are 2x more common. The base rate is 67% downside.

- The 1987 analog: Not saying March 2026 is October 1987. But the structure is the same: prolonged calm → upside breakout → ???

- What to watch: If the next 2-3 weeks produce multiple ±2% sessions, the volatility regime has shifted. Size down and widen stops.

Data: S&P 500, January 1950 – March 2026. A “low-volatility breakout” is defined as a day where the absolute return exceeds 2.85% after at least 90 consecutive trading days where no such move occurred.

日本語

日本語 Español

Español Português

Português العربية

العربية 繁體中文

繁體中文 简体中文

简体中文